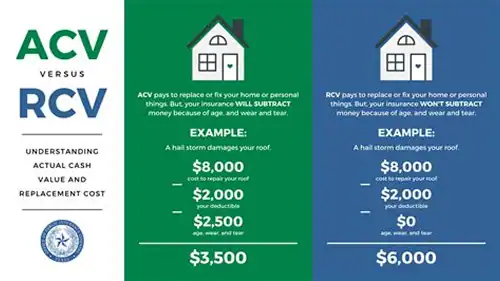

What’s the difference between Actual Cash Value and Replacement Cost in roof insurance?

The short answer: ACV pays the depreciated value of your roof, while RCV pays the full replacement cost. Here’s why that matters for San Antonio homeowners.

Actual Cash Value vs. Replacement Cost Roof Insurance: What Every San Antonio Homeowner Should Know

Most roof insurance policies will use either Actual Cash Value (ACV) or Replacement Cost Value (RCV) to calculate the payout for a roof damage claim. However, many homeowners don’t know the difference between these types of insurance—and it can make a huge difference when it comes to the out-of-pocket costs you may or may not wind up paying.

As San Antonio’s leading roofing experts, our team at Dolan Roofing & Construction has put together a full guide to Actual Cash Value and Replacement Cost insurance plans. Here’s what homeowners should know.

What Is Actual Cash Value (ACV)?

Actual Cash Value (ACV) coverage factors in depreciation, paying you only what your roof is worth at the time of damage—not what it costs to replace it brand new. In other words, if a roof originally cost you $15,000, but your insurance provider determines it’s lost 50% of its value due to age, they might only pay you $7,500 minus your deductible for a roof replacement.

While this may seem like a poor deal, there are both positives and negatives to an ACV policy. These policies usually have lower monthly premiums, which can make for a budget-friendly option. However, homeowners will face much higher out-of-pocket costs after making a claim.

What Is Replacement Cost Value (RCV)?

A Replacement Cost Value (RCV) policy covers the full cost to replace your roof with materials of like kind and quality. This policy type does not account for depreciation. While you’ll still pay a deductible, the insurance payout will be much higher—and closer to what you actually need to fully replace the roof.

The downside to an RCV policy is generally higher premiums. However, homeowners will enjoy greater financial protection in the event that their roof needs to be replaced unexpectedly.

Key Differences Between ACV and RCV

The main differences between Actual Cash Value and Replacement Cost Value lie in the overall coverage amount, the monthly premium costs, the out-of-pocket expenses, and each policy type’s suitability for older or newer roofs. Here’s how it all breaks down:

| Factor | Actual Cash Value (ACV) | Replacement Cost Value (RCV) |

| Coverage Amount | Pays the depreciated value of your roof at the time of damage. | Pays the full cost to replace your roof with materials of a similar kind and quality. |

| Premium Costs | Lower | Higher |

| Out-of-Pocket Expenses | Higher out-of-pocket costs as homeowners must cover the difference between the depreciated value and the new roof. | Lower out-of-pocket costs—usually just your deductible. |

| Suitability — Roof Age & Condition | Often more suitable for older roofs or tighter budgets. | Better for newer or well-maintained roofs. |

How These Coverage Types Affect Roof Insurance Claims

The main way that ACV vs. RCV insurance coverage will impact a roof insurance claim is in the amount of the claim settlement and the timing of the payments.

ACV policies will typically result in a reduced settlement in the form of a one-time payment. RCV policies, on the other hand, typically provide a higher settlement that is paid out in installments: the first being the Actual Cash Value of the roof, and the second being the depreciation after the roof has been replaced.

For more details on how Texas regulates homeowners’ insurance policies, see the Texas Department of Insurance for official guidance.

Which Option Is Right for You?

At Dolan Roofing & Construction, we almost always recommend replacement cost coverage—but there’s no one right answer when it comes to evaluating ACV vs. RCV for your roof and home. Here are some general rules of thumb.

✅ Choose ACV if:

- You’re comfortable covering more of the replacement cost out of pocket

- You want a lower monthly premium

- Your roof is nearing the end of its life

✅ Choose RCV if:

- You want full coverage for storm damage

- You prefer to pay more now to avoid large bills later

- You recently replaced your roof or plan to stay in your home long-term

Dolan Roofing & Construction Is Here to Help

Regardless of what insurance coverage you have, Dolan Roofing & Construction is here to be your go-to resource for navigating the insurance claim process and resolving roof storm damage.* Our team has years of expertise helping San Antonio document storm damage and ensure all damage is accounted for.

If you have any questions about your insurance policy, we recommend discussing it with your insurance provider. Then, when you need repairs due to storm damage, schedule an inspection with the experts at Dolan Roofing & Construction.

*Note: Dolan Roofing & Construction and its authorized representatives are NOT acting as Public Insurance Adjusters and will not negotiate with insurance on the Customer’s behalf.

Actual vs Replacement Cost Value FAQs

Can I switch from ACV to RCV coverage?

In many cases, yes—but it may require an inspection and an increase in your premiums. Policy changes are regulated at the state level, so check the Texas Department of Insurance for official guidance.

How does roof age affect insurance coverage?

Older roofs often default to ACV coverage, while newer roofs may qualify for RCV. In some cases, homeowners may have an ACV policy without knowing it—so be sure to check with your insurance provider.

What steps should I take after storm damage?

Contact your roofing contractor for an inspection, take photos, and notify your insurance company promptly.